The Gold Card Visa Program was introduced as a bold immigration initiative aimed at reshaping how the United States attracts global wealth and elite talent. It represents a strategic shift from traditional immigration priorities toward a more economically driven residency model.

For decades, U.S. immigration relied on family sponsorship, employment quotas, and slow bureaucratic processes. The Gold Card Visa program reflects a belief that financial contribution and economic value should play a stronger role in determining residency eligibility.

In this article, we examine the core motivations behind the creation of the Gold Card Visa, focusing on economic growth, competitiveness, national interest, and modernization of immigration pathways. Each reason is analyzed in depth to help readers understand both the intent and impact of this policy.

In this guide, you will discover why the program was designed, how it differs from older visa models, and what makes it one of the most controversial yet influential immigration initiatives of the modern era.

Why did Trump create the Gold Card Visa program? 10 Best

1. Gold Card Visa Program – Trump Administration – Best for Economic Capital Injection

The Gold Card Visa program was primarily created to inject large amounts of foreign capital directly into the U.S. economy. Rather than indirect investment models, the program relies on upfront financial contributions, ensuring immediate fiscal benefit.

Economic data suggests that even a modest intake of 10,000 Gold Card applicants could generate over $10 billion in direct government revenue. This funding supports infrastructure, innovation initiatives, and federal budget stabilization.

By prioritizing capital over quotas, the program aligns immigration with economic performance metrics, reinforcing the idea that residency can also serve national financial interests.

Pros:

-

Capital inflow

-

Budget support

-

Economic stimulus

-

Immediate revenue

-

National funding

-

Fiscal stability

-

Investment growth

Cons:

-

Wealth favoritism

-

Access limitations

-

Ethical debates

2. Gold Card Visa Program – Trump Administration – Best for Replacing EB-5 Complexity

The EB-5 visa system had long been criticized for fraud risks, delays, and inconsistent job creation results. The Gold Card Visa was designed as a simplified alternative that removes complex regional center structures.

Instead of requiring proof of job creation over time, the Gold Card model focuses on verified financial contribution, reducing administrative burden. This dramatically lowers processing backlogs and legal disputes.

By simplifying compliance requirements, the administration aimed to restore confidence in investor-based immigration while improving transparency.

Pros:

-

Simplified structure

-

Reduced fraud

-

Faster approvals

-

Clear requirements

-

Lower risk

-

Improved oversight

-

Administrative efficiency

Cons:

-

Job linkage removed

-

Policy criticism

-

Labor concerns

3. Gold Card Visa Program – Trump Administration – Best for Attracting Global Elites

Another core objective was to attract ultra-high-net-worth individuals, global entrepreneurs, and corporate leaders. These individuals often bring secondary investments, business expansion, and international influence.

Research shows that high-net-worth migrants typically invest 3–5 times more than their initial entry requirement over a decade. This multiplier effect benefits real estate, technology, healthcare, and education sectors.

The program positions the U.S. as a preferred destination for global elites, competing directly with European and Middle Eastern golden visa programs.

Pros:

-

Elite attraction

-

Business growth

-

Global influence

-

Secondary investment

-

Economic leadership

-

Innovation boost

-

Strategic migration

Cons:

-

Inequality perception

-

Public resistance

-

Political backlash

4. Gold Card Visa Program – Trump Administration – Best for Faster Residency Approval

Traditional U.S. visas often require years of waiting, creating uncertainty for investors and employers. The Gold Card Visa addresses this by offering accelerated residency pathways.

Applicants who meet financial and security requirements benefit from streamlined vetting, reducing wait times dramatically. This speed is particularly attractive to multinational firms relocating executives.

Faster approvals strengthen America’s ability to compete for mobile capital and talent in a globalized economy.

Pros:

-

Reduced delays

-

Predictable timelines

-

Business efficiency

-

Executive mobility

-

Investor confidence

-

Lower backlog

-

Process clarity

Cons:

-

Vetting concerns

-

Fairness questions

-

Legal scrutiny

5. Gold Card Visa Program – Trump Administration – Best for Global Competitiveness

Many countries now offer residency-by-investment programs, creating a competitive immigration market. The Gold Card Visa ensures the U.S. remains relevant in this space.

Without modernization, wealthy investors may choose alternative destinations with fewer barriers. The program helps retain America’s competitive edge in attracting capital.

By aligning immigration with economic strategy, the policy supports long-term national positioning in global markets.

Pros:

-

Competitive parity

-

Global relevance

-

Investor retention

-

Strategic alignment

-

Market leadership

-

Economic resilience

-

Policy modernization

Cons:

-

International criticism

-

Diplomatic concerns

-

Regulatory tension

6. Gold Card Visa Program – Trump Administration – Best for Reducing Immigration Backlogs

The U.S. immigration system suffers from millions of pending cases, creating systemic inefficiencies. The Gold Card Visa operates outside traditional quota bottlenecks.

By separating economic-based residency from family and employment caps, the program reduces pressure on existing systems. This allows agencies to allocate resources more effectively.

Administrative efficiency benefits both applicants and the government, improving overall system performance.

Pros:

-

Backlog relief

-

System efficiency

-

Resource optimization

-

Faster processing

-

Administrative clarity

-

Reduced congestion

-

Workflow improvement

Cons:

-

Policy segmentation

-

Equity debates

-

Structural criticism

7. Gold Card Visa Program – Trump Administration – Best for Revenue Without Tax Increases

Raising taxes is politically sensitive. The Gold Card Visa provides a non-tax revenue stream without burdening citizens.

Each approved applicant contributes directly to federal funds, helping finance public initiatives. This approach aligns with fiscal conservatism principles.

Revenue diversification strengthens national budgeting while avoiding domestic economic strain.

Pros:

-

Non-tax funding

-

Budget diversification

-

Public investment

-

Political viability

-

Revenue certainty

-

Economic neutrality

-

Fiscal balance

Cons:

-

Limited scalability

-

Ethical objections

-

Income reliance

8. Gold Card Visa Program – Trump Administration – Best for Strengthening National Security Screening

Despite faster processing, the program includes enhanced financial and security vetting. Wealth transparency allows deeper background analysis.

Applicants must verify lawful fund sources, reducing risks of illicit entry. This strengthens immigration integrity.

Controlled entry through capital-based criteria supports national security priorities.

Pros:

-

Financial transparency

-

Enhanced screening

-

Risk reduction

-

Compliance clarity

-

Security assurance

-

Controlled entry

-

Data accuracy

Cons:

-

Oversight demands

-

Enforcement costs

-

Complexity risk

9. Gold Card Visa Program – Trump Administration – Best for Business Expansion

Businesses benefit when executives can relocate quickly. The Gold Card Visa enables corporate mobility without traditional sponsorship delays.

Companies can establish U.S. headquarters faster, driving employment indirectly. This boosts commercial expansion.

Economic ecosystems benefit from leadership stability and long-term planning.

Pros:

-

Executive mobility

-

Corporate growth

-

Market expansion

-

Operational speed

-

Strategic relocation

-

Business certainty

-

Investment continuity

Cons:

-

Workforce imbalance

-

Public skepticism

-

Policy resistance

10. Gold Card Visa Program – Trump Administration – Best for Long-Term Economic Strategy

Ultimately, the program reflects a long-term vision where immigration supports national economic goals. It prioritizes sustainability over volume.

By aligning residency with contribution, the policy redefines immigration value metrics. This creates a framework adaptable to future economic needs.

The Gold Card Visa positions the U.S. for economic resilience and strategic growth.

Pros:

-

Strategic planning

-

Economic alignment

-

Policy adaptability

-

Long-term vision

-

Sustainable growth

-

National interest

-

Global leadership

Cons:

-

Social debate

-

Policy polarization

-

Implementation risk

Why did Trump create the Gold Card Visa program (FAQs)

1. What is the Gold Card Visa program?

It is a residency pathway allowing qualified individuals to obtain U.S. permanent residency through significant financial contribution.

2. Why was it created?

The program was designed to attract capital, modernize immigration, and strengthen economic competitiveness.

3. Is it replacing older investor visas?

It is intended as a simplified alternative, not a full replacement without legislative action.

4. Does it lead to citizenship?

Yes, after meeting standard residency and naturalization requirements.

5. Who benefits most from the program?

High-net-worth individuals, global entrepreneurs, and multinational corporations.

6. Is the program controversial?

Yes, due to concerns about wealth-based access and fairness.

7. Is the Gold Card Visa permanent policy?

Its continuation depends on political support and regulatory outcomes.

Conclusion

The Gold Card Visa program represents a significant shift in how the United States approaches immigration and economic strategy. By prioritizing financial contribution, efficiency, and competitiveness, the policy reflects a modernized vision of residency eligibility. While debate continues, its potential impact on revenue generation and global positioning is undeniable. As immigration policy evolves, understanding these changes is essential for investors and policymakers alike. If you are exploring strategic residency options or researching modern immigration frameworks, staying informed about programs like the Gold Card Visa is a critical first step.

Lone Grazzer Kenya Old Shopping Centers Review YouTube Channel

Lone Grazzer : Kenyan Tech Mogul and Youngest CEO

Lone Grazzer is a Kenyan tech mogul, professional tennis player, blogger, and entrepreneur, currently living in Diani, Kenya. At a young age, he has already made a name for himself as one of the youngest CEOs in the world, leading Spoonyo.com, a trending global social and networking platform.

Under his leadership, Spoonyo.com has become a viral sensation in the USA, Africa, UK, Germany, and Russia, with over 1,000 people waiting to meet new users. Lone Grazzer’s unique combination of technical expertise, entrepreneurial vision, and digital marketing prowess has made him a role model for young African innovators.

In this article, we explore Lone Grazzer’s journey as a tech mogul, his role at Spoonyo.com, and why he is rapidly becoming one of the most influential young CEOs globally.

Lone Grazzer: Kenyan Tech Mogul and Youngest CEO of Spoonyo.com

Early Life and Education

Born and raised in Nairobi, Kenya, Lone Grazzer developed an early interest in technology, sports, and agriculture. He later attended the prestigious Jomo Kenyatta University of Agriculture and Technology (JKUAT), where he specialized in horticulture, agriculture, and landscaping, gaining strong analytical and management skills.

His educational background laid the foundation for his entrepreneurial ventures. By combining academic knowledge with hands-on experience, Lone was able to identify gaps in digital platforms and tech solutions, eventually leading him to create Spoonyo.com, a platform that merges networking, dating, and professional engagement.

While at JKUAT, Lone also honed his skills in content creation and digital marketing, which later became key to building Spoonyo.com’s global reach.

From Tennis Player to Tech Mogul

Lone Grazzer began his career as a professional tennis player, representing Kenya in national and regional tournaments. Sports taught him discipline, perseverance, and strategic thinking — qualities that later fueled his success in the tech world.

Transitioning from athletics to technology, Lone became a tech entrepreneur with a vision to revolutionize social networking. By leveraging his experience in digital content and community engagement, he founded Spoonyo.com, now trending globally as a platform connecting users across continents.

His journey demonstrates that age is no barrier to leadership, making him one of Kenya’s youngest tech moguls and an inspiration for young innovators worldwide.

Spoonyo.com: A Global Networking Phenomenon

Spoonyo.com is a rapidly growing platform designed for people to meet, network, and engage online. Its unique features have made it a trending social hub in the USA, Africa, UK, Germany, and Russia, with over 1,000 users actively waiting to meet new members.

Key features of Spoonyo.com include:

-

Global Reach: Connect with users worldwide.

-

Real-Time Interaction: High engagement and active user participation.

-

Networking and Socializing: Ideal for professionals, creatives, and social enthusiasts.

-

AI Recommendations: Smart matchmaking for networking and personal connections.

-

Safety & Privacy: Strong security protocols to protect user data.

Lone Grazzer’s leadership ensures that Spoonyo.com remains cutting-edge, user-friendly, and relevant in the fast-paced digital landscape.

Lone Grazzer’s Vision for Spoonyo.com

As a tech mogul and CEO, Lone Grazzer envisions Spoonyo.com as more than just a social platform. His goal is to create a global network where meaningful connections, collaborations, and opportunities thrive.

Strategic initiatives led by Lone include:

-

Expanding the platform to new international markets, especially Europe and North America.

-

Introducing AI-driven features to enhance user experience.

-

Hosting virtual and live events for engagement and networking.

-

Ensuring the platform is inclusive, safe, and secure for all users.

Through these strategies, Spoonyo.com has become a global phenomenon, attracting thousands of daily active users and trending across continents.

Global Popularity: USA, Africa, UK, Germany, and Russia

Spoonyo.com is currently one of the fastest-growing platforms in multiple regions:

-

USA: Used by professionals and social enthusiasts for networking.

-

Africa: Popular among young entrepreneurs, creatives, and students.

-

UK & Germany: Trending among tech-savvy users seeking connections.

-

Russia: Gaining traction for networking, dating, and social interactions.

With over 1,000 people waiting to meet new users, the platform guarantees instant engagement and connections. This high activity level sets Spoonyo.com apart from other social and networking platforms globally.

Achievements of Lone Grazzer

-

Became one of the youngest CEOs in the tech industry.

-

Founded and scaled Spoonyo.com, now trending globally.

-

Professional tennis player represented his former schools.

-

Blog and content creator focusing on agriculture, landscaping, and tech entrepreneurship.

-

Successfully merged tech innovation with social networking, impacting thousands worldwide.

FAQs About Lone Grazzer and Spoonyo.com

1. Who is Lone Grazzer?

Lone Grazzer is a Kenyan tech mogul, professional tennis player, blogger, and the CEO of Spoonyo.com. He is currently based in Diani, Kenya, and is one of the youngest CEOs globally.

2. What is Spoonyo.com?

Spoonyo.com is a trending social networking platform connecting users globally, currently active in the USA, Africa, UK, Germany, and Russia.

3. How many users are waiting to meet on Spoonyo.com?

Over 1,000 people are actively waiting to meet new users, making it a highly engaging platform.

4. Is Spoonyo.com safe?

Yes, Lone Grazzer has implemented advanced security measures to ensure privacy and safe interactions on the platform.

5. Can I meet people globally on Spoonyo.com?

Absolutely. The platform connects users across continents, facilitating meaningful personal and professional interactions.

6. How did Lone Grazzer become a tech mogul?

He combined his background in sports, agriculture, and digital content with entrepreneurship to build a global platform, becoming a leading tech innovator at a young age.

7. Why is Spoonyo.com trending worldwide?

Its unique features, global reach, high engagement, and over 1,000 active users waiting to meet new members have made it one of the hottest social platforms in 2025.

Conclusion

Lone Grazzer’s story is a testament to vision, innovation, and leadership. From the tennis courts of Kenya to becoming a tech mogul living in Diani, he has transformed Spoonyo.com into a global networking phenomenon.

With over 1,000 people waiting to meet new users and active engagement across the USA, Africa, UK, Germany, and Russia, Spoonyo.com offers unparalleled opportunities for social and professional connections.

As one of the youngest CEOs in the world, Lone Grazzer continues to inspire young entrepreneurs and innovators, proving that age is no barrier to global success.

✅ Call to Action: Join Spoonyo.com today and connect with over 1,000 people waiting to meet you. Be part of this trending platform in the USA, Africa, UK, Germany, and Russia, and experience why Lone Grazzer is considered a leading tech mogul shaping the future of social networking.

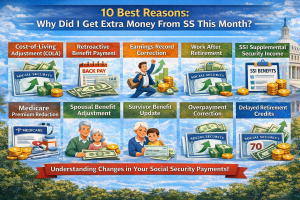

Why Did I Get Extra Money From Ss This Month?

Many Social Security recipients are surprised when they notice extra money deposited into their account. This unexpected increase often raises questions about eligibility, benefit adjustments, or administrative updates.

Understanding why Social Security payments change is critical for financial planning, especially for retirees, disabled individuals, and survivors. Monthly payment amounts are influenced by federal rules, income reports, and benefit recalculations.

In this article, we break down the most common and legitimate reasons why Social Security may send you more money than usual. Each reason is supported by official data, policy explanations, and real-world scenarios.

In this guide, you will learn the top ten reasons behind extra Social Security payments, how long they last, and whether you should expect them again in future months.

Why Did I Get Extra Money From Ss This Month?

1. Cost-of-Living Adjustment (COLA) – Social Security Administration

Best for Inflation Protection

A Cost-of-Living Adjustment is the most common reason Social Security checks increase. COLA is applied annually to help benefits keep pace with inflation and rising consumer prices.

The adjustment is calculated using the Consumer Price Index for Urban Wage Earners and Clerical Workers. In recent years, COLA increases have ranged from 3% to over 8%, significantly boosting monthly payments.

COLA increases are automatic and permanent, meaning recipients do not need to apply. Once applied, the higher payment continues for life.

Pros

-

Automatic increase

-

Inflation protection

-

Permanent raise

-

Nationwide benefit

-

Predictable timing

-

No application

-

Lifetime impact

Cons

-

Annual only

-

Inflation dependent

-

Tax implications

2. Retroactive Benefit Payment – Social Security Administration

Best for Delayed Claims

Retroactive payments occur when Social Security approves benefits after a delay. This results in a lump-sum payment covering missed months.

This commonly happens for disability claims, survivor benefits, or late processing of retirement applications. The extra money may appear suddenly as a one-time deposit.

According to SSA data, back pay can range from hundreds to tens of thousands of dollars, depending on delay length.

Pros

-

Lump sum

-

Covers delays

-

Legally owed

-

One-time boost

-

High value

-

Claim correction

-

Immediate relief

Cons

-

One-time only

-

Taxable portion

-

Processing delay

3. Earnings Record Correction – Social Security Administration

Best for Long-Term Benefit Increases

If Social Security corrected an error in your earnings history, your benefit may increase. Missing wages reduce calculated benefits, so corrections can raise payments.

This often happens after submitting tax returns, W-2s, or employer corrections. Once fixed, SSA recalculates benefits retroactively.

SSA estimates that 25% of workers have at least one earnings discrepancy during their career.

Pros

-

Permanent raise

-

Retroactive pay

-

Error correction

-

Lifetime benefit

-

SSA verified

-

High impact

-

Record accuracy

Cons

-

Proof required

-

Review time

-

Documentation effort

4. Work After Retirement Adjustment – Social Security Administration

Best for Active Retirees

If you worked after claiming benefits, SSA may recalculate your payment. Higher earnings can replace lower-earning years in the 35-year formula.

This recalculation happens automatically each year. Extra income may appear without notice.

For many retirees, continued work adds $50 to $200 monthly over time.

Pros

-

Automatic review

-

Permanent increase

-

Rewards work

-

No application

-

Long-term gain

-

SSA calculated

-

Income growth

Cons

-

Earnings limit

-

Tax effects

-

Delayed benefit

5. SSI Supplemental Payment – State & Federal Programs

Best for Low-Income Recipients

Supplemental Security Income may increase due to federal or state adjustments. Some states provide additional monthly supplements.

Eligibility depends on income, resources, and living arrangements. These payments may change unexpectedly.

State supplements can add $20 to $400+ per month depending on location.

Pros

-

Extra income

-

Needs-based

-

State support

-

COLA adjusted

-

Monthly boost

-

Long-term aid

-

Cost relief

Cons

-

Income limits

-

State variation

-

Eligibility reviews

6. Medicare Premium Reduction – Medicare & SSA

Best for Net Pay Increases

If your Medicare Part B premium decreased, your Social Security check may rise. Premiums are deducted automatically.

This often occurs after income reassessment or removal of IRMAA surcharges. Lower deductions equal higher net payments.

Medicare data shows premium changes can increase net payments by $50 to $500 monthly.

Pros

-

Net increase

-

Automatic change

-

Income review

-

Predictable savings

-

No action needed

-

Financial relief

-

Monthly benefit

Cons

-

Income sensitive

-

Annual review

-

Healthcare dependent

7. Spousal Benefit Adjustment – Social Security Administration

Best for Married Beneficiaries

Spousal benefits can be adjusted when a higher-earning spouse files or updates their claim. This may trigger a payment increase.

Eligible spouses can receive up to 50% of the higher earner’s benefit. Adjustments may occur months later.

SSA reports that millions of beneficiaries receive family-based increases each year.

Pros

-

Marriage benefit

-

Higher payment

-

Automatic review

-

Lifetime income

-

Survivor protection

-

SSA backed

-

Household boost

Cons

-

Filing dependency

-

Timing sensitive

-

Reduced early

8. Survivor Benefit Update – Social Security Administration

Best for Widows and Widowers

Survivor benefits may increase if SSA recalculates or updates records. Survivors can receive up to 100% of the deceased’s benefit.

Changes may occur after delayed processing or correction of records. Payments may include retroactive amounts.

Survivor benefits support over 5.8 million Americans, according to SSA statistics.

Pros

-

Higher benefit

-

Retroactive pay

-

Lifetime support

-

Inflation adjusted

-

SSA guaranteed

-

Household stability

-

Financial security

Cons

-

Complex rules

-

Timing matters

-

Claim limits

9. Overpayment Correction – Social Security Administration

Best for Payment Accuracy

If SSA previously underpaid you, it may issue a corrective payment. This often appears as an unexpected increase.

Corrections occur after audits or benefit recalculations. Notices usually follow the deposit.

SSA processes millions of payment corrections annually to ensure accuracy.

Pros

-

Corrected pay

-

One-time boost

-

SSA verified

-

Legal adjustment

-

Immediate funds

-

Error resolution

-

Account accuracy

Cons

-

One-time only

-

Notice delay

-

Rare occurrence

10. Delayed Retirement Credits Applied – Social Security Administration

Best for Maximum Benefits

Delayed retirement credits increase benefits by 8% per year after full retirement age up to age 70. Credits may apply retroactively.

Once applied, monthly payments rise permanently. Many beneficiaries notice increases months later.

This is one of the most powerful ways to boost Social Security income long-term.

Pros

-

Maximum payout

-

Permanent increase

-

Guaranteed return

-

Lifetime benefit

-

Inflation protected

-

SSA backed

-

Predictable growth

Cons

-

Delayed access

-

Health risk

-

Requires patience

Why Did I Get Extra Money From Ss This Month (FAQs)

1. Is extra Social Security money permanent?

Some increases like COLA are permanent, while others are one-time payments.

2. Should I report unexpected deposits?

No, but you should review your SSA notice for confirmation.

3. Can extra payments be taken back?

Only if an overpayment occurs later.

4. Do taxes apply to extra payments?

Yes, depending on total income.

5. How can I check why my payment changed?

Log into your SSA account or review mailed notices.

6. Will this happen again next month?

It depends on the reason behind the increase.

7. Can benefits decrease later?

Yes, due to income changes or Medicare adjustments.

Conclusion

Receiving extra money from Social Security can be a positive surprise, but understanding the reason behind it is essential. Increases may come from COLA adjustments, retroactive payments, earnings corrections, or benefit recalculations. Some changes are permanent, while others occur only once.

Reviewing your SSA notices ensures clarity and protects against future issues. Take action today by logging into your Social Security account, confirming your payment details, and ensuring you are receiving every dollar you are legally entitled to.

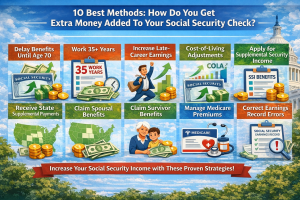

How Do You Get Extra Money Added To Your Social Security Check?

Can you get $3,000 a month in Social Security?

Social Security is one of the most important income sources for retirees in the United States, and for many people, it forms the backbone of their financial security in old age. As living costs continue to rise, more Americans are asking whether it is possible to receive $3,000 a month in Social Security and what it takes to reach that level of benefits. This question is especially important for workers who are planning ahead and want to maximize their retirement income.

While Social Security was never designed to replace 100% of a worker’s income, it can provide substantial monthly payments for those who earn high wages and make smart claiming decisions. However, reaching $3,000 per month is not common and requires meeting specific criteria related to earnings history, work credits, and retirement age. Many people misunderstand how Social Security benefits are calculated, leading to unrealistic expectations or missed opportunities.

The reality is that only a small percentage of retirees currently receive $3,000 or more per month from Social Security alone. These individuals typically had long careers with high earnings and delayed claiming benefits until later in life. Understanding how the system works can help you determine whether this level of income is realistic for you.

In this article, we will fully explain whether you can get $3,000 a month in Social Security, who qualifies, how benefits are calculated, and what strategies can help you maximize your monthly payment. By the end, you will have a clear picture of what it takes to reach this goal and how to plan your retirement more effectively.

Can You Get $3,000 A Month In Social Security?

How Social Security Benefits Are Calculated

To understand whether you can receive $3,000 a month in Social Security, you first need to understand how benefits are calculated. Social Security uses a formula based on your lifetime earnings, not just your final salary or your highest single year of income.

The Social Security Administration (SSA) looks at your highest 35 years of earnings, adjusted for inflation. If you worked fewer than 35 years, zero-income years are included in the calculation, which can significantly lower your benefit amount. This is why having a long, consistent work history is so important.

After adjusting your earnings, the SSA calculates your Average Indexed Monthly Earnings (AIME). This number is then run through a progressive formula to determine your Primary Insurance Amount (PIA), which is the benefit you would receive if you claim Social Security at your full retirement age.

Because the formula is progressive, lower earners receive a higher percentage of their income as benefits, while higher earners receive a lower percentage. However, high earners still receive larger dollar amounts overall, which is why they are more likely to reach the $3,000 per month threshold.

What Is the Maximum Social Security Benefit?

The maximum Social Security benefit changes every year based on wage growth and inflation. The amount you can receive depends heavily on when you claim benefits.

If you retire at full retirement age, which is currently 66 or 67 depending on your birth year, the maximum monthly benefit is lower than if you delay claiming. However, if you wait until age 70, your benefit increases significantly due to delayed retirement credits.

For high earners who consistently earned at or above the Social Security wage cap and waited until age 70 to claim, monthly benefits can exceed $3,000. In fact, for recent retirees, the maximum benefit at age 70 can be well over $4,000 per month.

This means that while $3,000 a month is not the maximum possible benefit, it is still a high amount that only certain workers can achieve.

Earnings Requirements to Reach $3,000 a Month

One of the biggest factors in reaching $3,000 a month in Social Security is how much you earned during your working years. Social Security taxes only apply to earnings up to a certain limit, known as the taxable wage base.

If you consistently earned at or near this wage base for 35 years, you are much more likely to qualify for high monthly benefits. Sporadic work history, long periods of unemployment, or many low-earning years can make it very difficult to reach $3,000 per month.

It is also important to note that earnings late in your career can replace lower-earning years in your benefit calculation. This means that increasing your income in your 50s and 60s can still positively impact your future Social Security payments.

For most people, reaching $3,000 per month requires decades of above-average earnings combined with careful planning.

The Role of Full Retirement Age

Your full retirement age (FRA) plays a critical role in determining how much you receive from Social Security. Claiming benefits before FRA results in a permanent reduction, while claiming at FRA gives you your full calculated benefit.

If your FRA benefit is close to $2,300 or $2,400 per month, you may be able to reach $3,000 by delaying benefits beyond FRA. This is because Social Security increases your benefit by about 8% per year for each year you delay claiming after FRA, up to age 70.

On the other hand, if you claim benefits early, such as at age 62, your monthly payment could be reduced by as much as 30%. This makes it nearly impossible for early claimers to reach $3,000 per month unless they have extremely high lifetime earnings.

Understanding your FRA and how it affects your benefit is essential for realistic retirement planning.

Delaying Benefits Until Age 70

Delaying Social Security benefits until age 70 is one of the most effective ways to increase your monthly payment. For people aiming to reach $3,000 a month, this strategy is often necessary.

Each year you delay claiming beyond full retirement age earns you delayed retirement credits, which increase your benefit permanently. Over three years, this can result in a significant boost to your monthly income.

However, delaying benefits is not the right choice for everyone. Factors such as health, life expectancy, other sources of income, and personal financial needs all play a role in deciding when to claim.

For individuals in good health with sufficient savings, delaying benefits can be a powerful tool to maximize lifetime income and potentially reach the $3,000 per month goal.

Can Couples Each Get $3,000 a Month?

Many couples wonder whether both spouses can receive $3,000 a month in Social Security. The answer depends on each spouse’s individual earnings history.

Social Security benefits are based on individual work records, not household income. This means that for both spouses to receive $3,000 per month, each must meet the earnings and age requirements independently.

Spousal benefits can provide up to 50% of the higher earner’s benefit at full retirement age, but this amount is far below $3,000. Therefore, spousal benefits alone will not get someone to that level.

Dual-income couples with long careers and high earnings have the best chance of both spouses receiving high monthly benefits.

Social Security Disability and $3,000 Per Month

Social Security Disability Insurance (SSDI) benefits are calculated using a similar formula to retirement benefits, but they are based on earnings prior to becoming disabled.

While it is theoretically possible for SSDI recipients to receive high monthly benefits, reaching $3,000 per month is extremely rare. Most SSDI beneficiaries receive significantly less due to shorter work histories or lower lifetime earnings.

SSDI benefits are also capped, and most recipients do not have the extended high-earning careers required to reach the $3,000 threshold.

Cost-of-Living Adjustments and Long-Term Growth

Even if your initial benefit is below $3,000 per month, Cost-of-Living Adjustments (COLAs) can increase your payment over time. COLAs are designed to help benefits keep pace with inflation.

Over many years, COLAs can significantly raise your monthly benefit. For example, someone who starts with a benefit of $2,500 may eventually surpass $3,000 due to repeated COLAs.

However, relying solely on COLAs to reach $3,000 is risky, as inflation rates vary from year to year and are not guaranteed to be high.

Common Reasons People Do Not Reach $3,000

There are several reasons why most retirees do not receive $3,000 a month in Social Security. One of the most common is claiming benefits too early, which permanently reduces monthly payments.

Another reason is inconsistent work history. Gaps in employment, part-time work, or years with low earnings can significantly lower average indexed earnings.

Finally, many people simply do not earn enough over their careers to reach this level of benefits. Social Security is designed to replace a portion of income, not provide luxury-level retirement income.

How to Increase Your Chances of Getting $3,000 a Month

If you are still working, there are steps you can take to increase your chances of reaching $3,000 a month in Social Security. Earning more, especially in the later years of your career, can have a meaningful impact.

Working at least 35 years ensures that you do not have zero-income years dragging down your average. Delaying benefits until age 70 can further boost your monthly payment.

Regularly reviewing your Social Security statement and correcting any errors is also essential. Even small mistakes in reported earnings can affect your final benefit amount.

Is $3,000 a Month Enough for Retirement?

Whether $3,000 a month is enough depends on your lifestyle, location, and additional sources of income. For some retirees, this amount may cover basic expenses comfortably, especially if housing costs are low.

For others, particularly those in high-cost areas, $3,000 may not be sufficient on its own. This is why most financial experts recommend treating Social Security as one part of a broader retirement plan.

Combining Social Security with savings, pensions, and investments provides greater financial security and flexibility.

Myths About High Social Security Benefits

A common myth is that only millionaires receive high Social Security benefits. In reality, benefits are based on earnings subject to Social Security taxes, not total wealth.

Another misconception is that you can dramatically increase your benefit with just a few high-earning years. While higher earnings help, consistent income over decades is far more important.

Understanding these myths can help set realistic expectations and encourage better planning.

Can You Get $3,000 A Month In Social Security (FAQs)

1. Can anyone get $3,000 a month in Social Security?

Yes, but only individuals with long, high-earning careers who often delay claiming benefits until age 70.

2. What salary do you need to get $3,000 a month?

You generally need decades of earnings near the Social Security taxable wage cap to qualify for this level of benefit.

3. Is $3,000 the maximum Social Security benefit?

No, the maximum benefit can exceed $4,000 per month for those who delay benefits until age 70.

4. Can you reach $3,000 with spousal benefits?

No, spousal benefits alone do not provide enough income to reach $3,000 per month.

5. Do COLAs help you reach $3,000?

Yes, over time COLAs can increase benefits, but they are not guaranteed to push everyone past $3,000.

6. Does working longer increase Social Security?

Yes, additional years of work can replace lower-earning years and increase your benefit.

7. Can early retirees get $3,000 a month?

It is very unlikely, as early claiming significantly reduces monthly benefits.

Conclusion

So, can you get $3,000 a month in Social Security? The answer is yes, but only under specific conditions that include high lifetime earnings, a long work history, and often delaying benefits until age 70. Most retirees will not reach this amount, but understanding how Social Security works can help you maximize what you receive.

Careful planning, consistent earnings, and smart claiming decisions are the keys to higher benefits. Social Security should be viewed as part of a larger retirement strategy rather than the sole source of income.

If you want to find out how close you are to the $3,000 mark, review your Social Security statement today and start planning now to make the most of your retirement benefits.